What You Need To Know About Getting A Mortgage

Securing a mortgage is one of the most important steps in the process of buying a new home. Whether you're investing in a real estate property or purchasing a home for you and your family to live in, the use of financing looms large in the overall equation. Rocket Mortgage reports that most buyers use a mortgage to fund their real estate purchase. This makes lending options a priority in any consideration of a new home purchase. Understanding the factors that determine eligibility and eventual interest rates and term options is a must for anyone in the market for a new property.

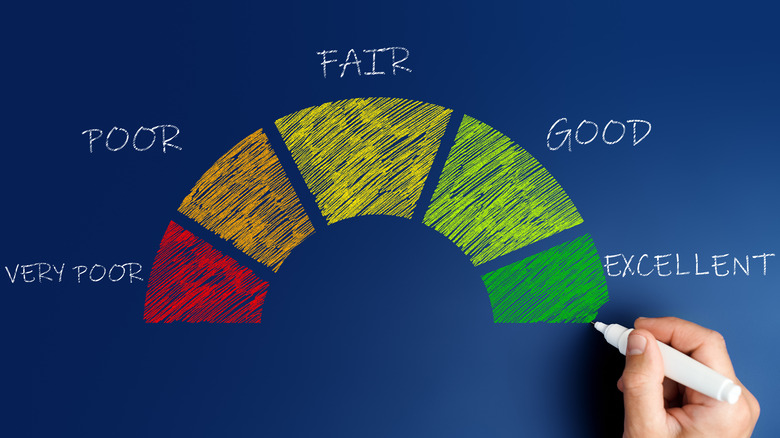

Debt.org notes that credit scores offer a tangible starting point for any lender who is evaluating your suitability as a borrower. This is a great place to begin for a borrower as well. In the months — or even years — leading up to a new purchase in the real estate market, you should get serious about caring for your credit score and existing credit accounts. Reducing the overall amount that you owe to existing lenders and keeping revolving lines of credit free can help you increase your score over the months that follow and can make a huge impact on your financing options.

Mortgages hinge on great planning. With these key pieces of information in your calculation, you can easily make the most of the lending process and walk away with a fantastic lending product that facilitates the lifestyle and home that you're seeking.

Start with your credit score

Caring for your credit score is a complex task. There are a considerable number of factors that play a role in pushing your credit score higher or lower over the course of many months and years, and most can be carefully calibrated for maximum impact. Your score is generally situated between a range from 300 to 850, according to Equifax. Good (670-739), very good (740-799), and excellent (800+) credit scores will always yield the best opportunities for low-cost lending products.

The length of your credit history is a good place to start when thinking through your current score. The longer you've been borrowing (and repaying your debts), the more likely a lender is to extend a new line of credit or personal loan to you. The length of your credit history shows a pattern of care in the world of consumer borrowing and will stand to you as you approach a new mortgage loan opportunity.

While the length of your credit history isn't something you can actively change, all the remaining features are within your control. Namely, the most important thing you can do to positively impact your credit is a balance of aggressive repayments and minimal utilization. Low revolving credit utilization is a sure sign of responsible borrowing in the eyes of virtually all lenders, says The Motley Fool.

Calculate your debt to income ratio and make necessary adjustments

Your debt to income ratio (DTI) is an incredibly important calculation to make as you begin to think about borrowing to pay for a new home. Wells Fargo notes that a debt-to-income ratio of 35% or less is ideal when approaching a lender for new funding. This means that 35% or less of your gross income is spent on your current rent or mortgage payments, credit card bills, and other routine debts that must be accounted for each month in your ongoing financial calculations.

A lower debt to income figure means greater fiscal mobility when it comes to saving, emergency spending, or increased borrowing (that comes along with elevated monthly repayment obligations). The lower this figure is, the more likely you are to be able to continuously afford your lifestyle.

Taking time to calculate this ratio before approaching your bank in search of a loan will give you a good bearing on your overall financial wellness. If you add up all your expenses and find that your DTI figure is in the 40s instead of the 30s, taking steps to reduce your outgoing expenses (renegotiating your electricity or television bill, moving to a cheaper apartment, or paying off a greater chunk of existing debts) before pursuing a loan can help you get the best rate on your new mortgage.

Save up for the down payment

Down payment cash is a must when hunting for the perfect home. The Mortgage Reports lists typical down payment figures based on age groups, noting that the average across all buyers in the United States is 12%, while those in their 20s average just 6% on their down payments. Lenders will hold unique criteria for extending a loan offer to borrowers based on many different factors, and the same goes for the down payment figure.

Whether you're aiming for a more traditional 20% down payment or seeking a minimized contribution to the overall sale price, the need to save up for the expense remains equally important. FRED reports that the average sale price on homes sold in the first quarter of 2022 was $507,800, meaning that a 6% down payment will cost just over $30,000 (while a 20% figure will lift the down payment to over $100,000).

Budgeting for your personal savings goal is crucial when seeking a mortgage to purchase your own home. Many people save for years to build up the cash reserve needed to transition into homeownership. Taking the time to understand your own budgetary restrictions and ability to save will help you create an attainable goal and a reasonable timeframe that serves your needs.

Make sure you seek out preapproval to make the buying process easier

Preapproval has become a gold standard in borrowing and house hunting these days. Seeking preapproval for a mortgage helps you approach real estate agents and sellers with confidence, and this step will help you solidify a budget that works for your financial standing, according to Rocket Mortgage. Often, house hunters who don't seek out preapproval on their future mortgage will ballpark a figure that they can afford, only to later find out that a bank will only loan them a fraction of the capital they need to complete the purchase of their dream home.

Investing time, energy, and emotion into the search for your next home is a standard practice, and when an opportunity falls through because of financing issues, buyers can easily become heartbroken, thinking that their only shot at finding the perfect home has passed through their fingers. Preapproval helps minimize these issues by providing the key resources necessary to understand your budget — and the budget that a lender will accept as a part of your efforts to purchase a new property.

Finalize your loan terms, focusing on rates, timelines, and other features

Hammering out the details is all about understanding the various components of a new loan agreement. The most important features in a mortgage loan are the interest rate, type of loan rate (variable versus fixed), and the length of time the loan will remain due. A 15-year, fixed-rate mortgage, for instance, will remain fixed at a set interest rate over the course of a 15-year period.

Debt.org notes that more than 85% of mortgage loans originated in 2016 were 30-year, fixed-rate mortgages. This option is immensely popular because it sets the repayment figure in stone and maintains one of the lowest possible monthly payment figures that a borrower will find on the market. A shorter loan duration (15 or 20 years terms, for instance) will see the mortgage loan paid faster, of course, but in order to accomplish this, you'll have to pay more each month to account for the shorter timeframe.

Many borrowers are happy to extend their repayments over a 30-year term and typically benefit from no prepayment penalties baked into the loan agreement, meaning that a faster overall payoff of the loan is possible but not mandated in the loan agreement.